A Roth conversion is a common term thrown around, but we wanted to detail out some of the particulars related to this and how we utilize them across our client base.

First, a brief overview of some of the differences between a Traditional IRA and Roth IRA. We are writing this on the assumption that the client is over the income limits for direct to Roth IRA contributions and do not qualify for a Traditional IRA contribution that is deductible.

Traditional IRA

• Contributions can be tax deductible or non-tax deductible (depending on income limits, access to a retirement plan and other factors)

• Value of account grows tax free

• Qualified distributions (over age 59.5 for example) are taxed at your ordinary income tax rate

• Required Minimum Distributions are required (RMD) and start depending on the year you were born

Roth IRA

• Contributions are made with after tax dollars or via a Roth conversion as we are discussing today

• Value of account grows tax free

• Qualified distributions (over age 59.5 for example) are tax free

• No Required Minimum Distribution

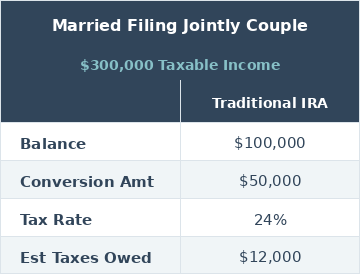

Non-Backdoor Roth Conversion Example

The objective here is to convert Traditional IRA funds (deductible contributions) to the Roth IRA. Because the contributions were originally tax deductible, all of the funds are taxable upon the conversion. There is no limit to the conversion amount or frequency, but the IRS will have your tax bill waiting for you. The dollars converted are added onto your taxable income. Caution is required here as this can push you into a higher tax bracket. Example below:

Backdoor Roth Conversion Example

Assuming you are over the income limits to directly contribute to a Roth IRA, we have to go about getting funds into your Roth IRA via a Roth conversion but with non-deductible Traditional IRA contributions. For example, you put $7,000 into your Traditional IRA and record it on your tax return as a non-deductible contribution for that tax year. You then convert the $7,000 to your Roth IRA while it is still in cash (not invested). The $7,000 is now your basis. Because there was no growth on the $7,000, you generally have a $0 tax bill on this conversion.

For illustration purposes only: contributing $7,000 annually over 25 years at a hypothetical 7% annual growth rate would produce approximately $442,743. This is a mathematical illustration, not a projection of actual results. Actual returns will vary and could be higher or lower. The 7% rate is not guaranteed and does not represent any specific investment.

What if you have a monthly auto deposit into your Traditional IRA and invest the funds throughout the year? Let’s assume the $7,000 basis (your total contributions) grows to $7,500 by the end of the year. Then you will pay taxes on the growth above your basis ($500) when you file your tax return. Side note for spouses, as long as one spouse has income, both spouses can participate in maxing out their annual IRA contributions.

Potential Pitfalls

The most common is the “pro-rata rule.” Note how the first example clearly states, deductible contributions. Let’s say you had $100,000 in your Traditional IRA (all deductible contributions) and decided to make a $7,000 non-deductible contribution and then immediately convert the $7,000. The IRS will now force you to use the “pro-rata” rule. This calculates the total value of all of your non-Roth IRA’s (Traditional, SEP, and SIMPLE) and provides you with an additional taxable amount on the conversion. Extreme caution must be exercised here as not understanding the pro-rata rule is the most common and costly mistake.

Potential Solution to Deductible IRA Funds

A common problem is you have rollover IRA funds from previous employers in your Traditional IRA. Let’s say you start with a new employer or you are a practice owner and launch a 401(k) for you and your employees. Most 401(k) plans allow for rollovers into a plan. So, you could take your Traditional IRA funds and roll those into the new 401(k) plan (assuming they are all tax-deductible contributions). Assuming you have no other non-Roth IRA’s, you can now utilize the “Backdoor Roth” strategy without fear of violating the pro-rata rule.

Takeaways

KEY TAKEAWAYS

• Annual non-deductible IRA contributions and subsequent Roth conversions can really enhance your tax-free savings bucket over the years.

• Caution must be exercised, especially around the pro-rata rule. Not understanding it is the most common and costly mistake.

• When appropriate, this strategy creates a tax-free bucket of money for retirement even though most are above the income limits for direct to Roth contributions. As always, consult your Advisor and CPA before utilizing these strategies.

If questions on your personal situation outside of your Annual Review, please reach out to your Advisor directly. For non-clients with questions on your personal situation, use the link below to reach out to us and an Advisor will contact you to schedule a complimentary consultation.

Virtus Financial Partners is a registered investment advisor specializing in comprehensive financial planning for dental professionals. The firm serves clients nationwide from its office in Winter Park, Florida.

Virtus Financial Partners is an investment advisor registered with the U.S. Securities and Exchange Commission. Any statement of past performance is not indicative of future returns. Virtus does not provide legal or tax advice. You should consult with your attorney or tax professional for any advice pertaining to legal and/or tax questions you have.