For many of our clients, the rise in interest rates the past few years is a new phenomenon for them. The Federal Reserve controls interest rates and uses them as a tool to manage the overall growth of the economy. Higher interest rates mean higher borrowing costs but also higher yields/returns on your excess cash.

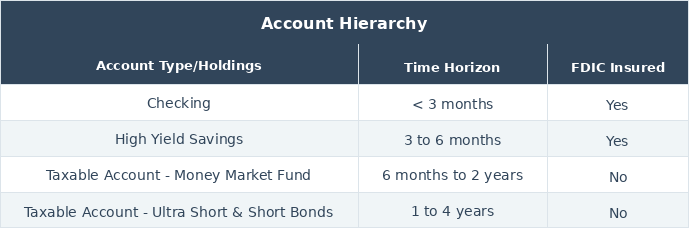

For today’s discussion we are going to look at the hierarchy of accounts for an example client. From risk free FDIC insured accounts to nominal risk in taxable accounts, the underlying components of these accounts, and throw in a tax equivalent yield calculation example.

In the chart above, the first two accounts are as risk free as we can get since they are FDIC Insured. Once you have reached your target amounts for those accounts and you have automated long-term investing (401(k), IRAs, etc), you might have excess cash that you do not have a specific objective for in the next few years. We see this a lot with our clients (especially business owners) that have too much cash on hand. The challenge is to balance return expectations, risk, and liquidity. Meaning, if we have cash we plan on using in the next 2 years, putting it all in a Technology ETF is probably not the most prudent decision. So, we start by looking at Treasury Bills/Notes/Bonds (guaranteed by the Federal Government) along with other areas of the fixed income market to add balance risk and potential return. Let’s go through the examples below as an option for putting your cash to work:

Taxable Account - Money Market Fund

A Money Market Fund is a Mutual Fund that invests in short-term, higher quality securities. Its goal is to maintain a Net Asset Value (NAV) of $1.00 which provides a high degree of liquidity (quick access to your money), stability of principal ($1.00 NAV) and typically higher yields (interest earned) than your bank account.

Types of Money Market Funds

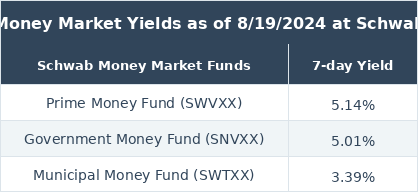

1. Prime Money Fund - Invests in high-quality, short-term money market securities issued by U.S. and foreign entities including corporations, financial institutions, and the U.S. Government.

2. Government Money Fund - Invests in short-term U.S. government debt with holdings in U.S. Treasury obligations or repurchase agreements.

3. Tax-Exempt Money Fund (Municipal Money Market Fund) - Invests in short-term municipal money market securities issued by states, local governments, and other municipal agencies.

Money Market Fund Maturities

The funds are regulated by the SEC and are required to maintain a weighted average maturity period of 60 days or less. This means that all of the underlying securities in the fund as a weighted average cannot mature more than 60 days. As an investor, this helps provide liquidity as there is constant turnover in the fund.

What is the 7-day Yield?

A method of estimating the annualized yield (payout) of a money market fund. This yield is net of any fund expenses (expense ratio). Keep in mind that the yield is affected by rates set by the federal reserve. So, if the fed cuts rates you would see this yield reduced over time.

Why use this investment option over my High Yield Savings Account?

Yields can be slightly higher and for individuals with large cash positions, every % point counts.

Taxable Account - Ultra and Short-Term Bonds

First off, let’s start off with the basics on what a bond is. In its most basic form, it is a loan taken out by a company and the money for the loan comes from investors. In return, the investors receive an interest coupon typically annually or semi-annually. On the maturity date the principal is returned (as long as the company doesn’t default on its bonds) and ending the loan.

Ultra Short-Term and Short-Term Meaning

• Ultra Short-Term Bonds - Generally defined as higher quality bonds that mature within 1 year

• Short-Term Bonds - Generally defined as bonds that mature in 1-3 years

What is the objective here?

The goal is to seek out a higher yield/return than a Money Market Fund but without taking on too much additional risk. By using shorter duration bonds, you are trying to lessen the risk of interest rate risk or credit risk.

How is this strategy implemented?

• Buying individual bonds to create your own bond ladder

• Using actively or passively managed ETFs or Mutual Funds (our preference is ETFs because of the tax efficiency) to create a strategy

• Using specified maturity ETFs to create a bond ladder

How do we use this for our clients?

Let’s say a client’s emergency savings is well funded, long-term investments are fully funded, and they still have extra cash. They don’t have any plans for at least 2-3 years for this cash but want to keep it liquid. We would tailor a strategy to match the client time horizon and current tax bracket (to decide on taxable bonds or municipal). We can then estimate the yield (interest paid by the bond or bond fund) over that time period. Remember although the duration reduces the risk, there still is risk and this is why this is the last account in the first chart for your cash.

Tax-Equivalent Yield

The purpose of this is to understand the return a taxable bond needs (treasuries, corporates, etc) for its yield to equal the yield on a comparable tax-exempt municipal bond based on your marginal tax bracket. There are many other factors to consider before making a decision and this is just an example of a specific calculation.

What is a taxable bond vs a tax-exempt municipal bond?

• Taxable Bond - A bond whose return to the investor is subject to taxes at the local, state, or federal level, or some combination thereof

• Tax-Exempt Municipal Bond - A bond issued by local, county, and state governments that is often tax free and can be an option for individuals in higher tax brackets

Example: You are a single individual in the 32% tax bracket for 2024 ($191,951 to $243,725). A tax-free bond is yielding 3%. Based on the formula: R(te) = 3% / (1-32%) = 4.41%. Tax-Equivalent Yield = 4.41%

What does this mean?

If an investor has access to a taxable bond yielding 5% or a tax-free bond yielding 3% and they are in the 32% tax bracket, the investor would be better off investing in the taxable bond even after paying their tax liability.

A lot to take in, but how you allocate your cash across your household is critical to creating efficiency. Every dollar that is not needed in the very short term for expenses should be put to work in a manner that maximizes the outcome while managing the risks.

Virtus Financial Partners is an investment advisor registered with the U.S. Securities and Exchange Commission. Any statement of past performance is not indicative of future returns. Virtus does not provide legal or tax advice. You should consult with your attorney or tax professional for any advice pertaining to legal and/or tax questions you have.