This is probably the fifth year in a row that there has been some monumental change on student loans that needs to be dissected for the D4's entering the workforce. The good old days were REPAYE for three years, then refinance. I'm over it, but it is important you understand the changes, so read on.

Let's go through some basics first, then the changes, and then a few examples. This is a long article, but there was a lot to cover.

The Basics

Regardless of whether you have federal or private loans coming out of school, we use three criteria that dictate how you manage your loans: career path, income, and interest rates. All three are affected by timing.

Career Path

Coming out of school, your plans and timing around your career are the gatekeeper to how we address your loans. A D4 going into a one-year GPR will require a different strategy than a D4 entering private practice with no desire to own. We can use this to project income into the future and how it will affect your loan repayment plan.

Income

Until you know what your income will consistently look like through the years, it is challenging to make a long-term decision between the IDR route (Income-Driven Repayment, the federal umbrella of plans) and refinancing. On an IDR path, your income dictates your payment. As your income ramps up, your payment increases. Once you reach a certain threshold, we can compare the total cost of your loans on the federal system to a refinance — paying your loan directly to a bank for a set rate and term.

Interest Rates

Once you have a clear idea of your career path and expected income, interest rates come into play. For the 2026 graduating class, weighted average federal loan rates are approximately 8% as of May 2026. We have seen clients refinance in the 4% to 6% range over the same period, depending on creditworthiness and lender.*

For example, if you have $400,000 in student loan debt, let's assume the weighted average interest rate is 8% and your income puts you on a 20-year payoff trajectory on a federal loan plan. Your total cost is $802,982. Take that same set of loans at a 5% interest rate over 20 years, and the total cost is $633,557 — a difference of $169,425. These figures are hypothetical illustrations; individual results vary.

Obviously, there are nuances to every situation, but if a borrower's income is high enough that they will pay off their loans within the federal system, then not evaluating a refinance would mean leaving meaningful savings on the table. Keep in mind that refinancing federal loans into a private loan permanently forfeits federal benefits — income-driven repayment, loan forgiveness, deferment and forbearance options, and death and disability discharge — so the savings must be weighed against the value of those protections. This cannot be done until your career path, income, and interest rates are in an optimal spot.

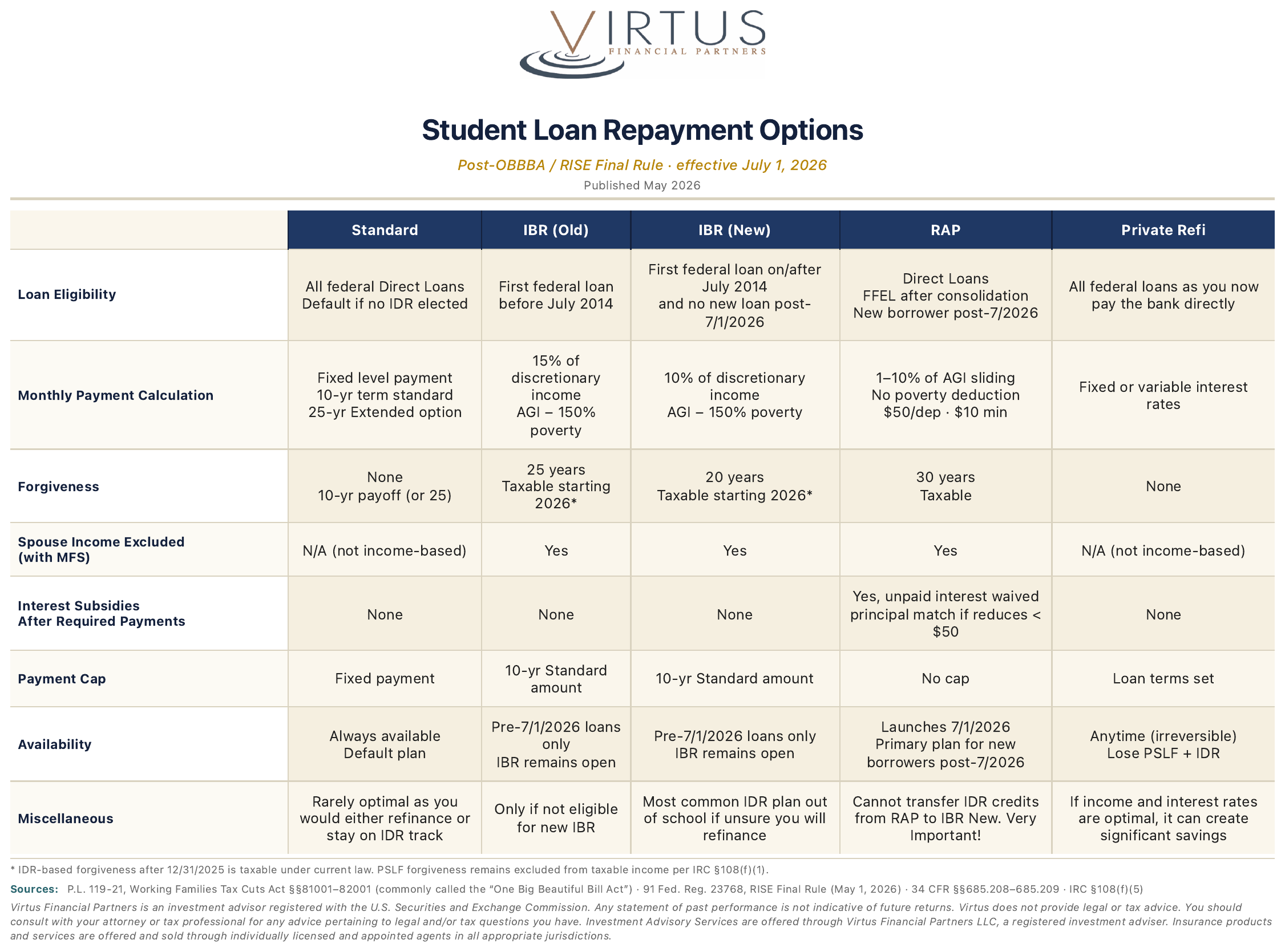

Your IDR Options Coming Out of School

With the recent changes, and assuming you are not borrowing or consolidating after 7/1/2026, here are your options:

• Old IBR — if your first loan was taken out prior to 7/1/2014.

• New IBR — if your first loan was taken out after 7/1/2014.

• Repayment Assistance Plan (RAP) — this plan is not live until 7/1/2026.

• Standard (existing 10-year) — although technically available, it is rarely used in an environment where interest rates favor a refinance (i.e., now).

The chart below compares the plans. Click it to open the full-size, more readable version:

No IDR Credit Transferability from RAP to IBR New

This is the big one. IDR credits accrued on RAP cannot be transferred to other plans. IDR credits are the time you have accrued toward the forgiveness period of the plan you are on.

Say you graduated in May 2026 with $400,000 in federal loans and you are making $180,000 as an associate. You start on RAP, assuming you will refinance as your income goes up. Fast-forward four years: your income has not gone up, and a refinance doesn't make sense because you can't handle the monthly payment. You decide to switch to IBR New to go for the 20-year forgiveness. Your IDR credits from RAP do not transfer, so you start over — and now it takes 24 years until your loans are forgiven.

This means your choice coming out of school this year is very important. You really have to understand why you are choosing the RAP plan and the ramifications if you do. There is a unique planning opportunity here that I will touch on later.

Taking Out Additional Federal Loans After 7/1/26

There are two issues with the new borrowing rules. The first is the new borrowing limits for professional loans (dental school and residency). If you are a current dental student with disbursements before 7/1/26, you retain Grad PLUS access through completion of your dental program. If you are a new borrower, or in another way starting a new program (a tuition-based pediatric residency, for example), you are subject to the new professional limits.

• Professional borrowers (dental, medical, law): $50,000 annual limit and $200,000 aggregate limit.

• Overall lifetime cap (most borrowers): $257,500.

New limits apply to periods of enrollment beginning on or after 7/1/26.

The Post-7/1/26 Repayment Plan Issue

Here is the big one. If you take out a loan after 7/1/2026 (existing dental students, new borrowers, or those starting or already in a tuition-based residency), the only plans you are eligible for coming out of your program are RAP, Old IBR, or Tiered Standard.

The issue is that you lose access to IBR New, which is a 20-year repayment plan, versus RAP, which is 30 years. To make it even more confusing, you can access Old IBR for the pre-7/1/2026 loans only. This is a game changer, because you have to make 10 more years of payments and your cost toward forgiveness goes up substantially.

For a lot of you there is no way around this, as you need both federal and private borrowing. For some, you might be able to take private loans only for your final year to maintain IBR New access. That is a planning opportunity.

Overall, this will more than likely force more borrowers to refinance and pay their loans off traditionally rather than planning on 30-year forgiveness, as the refinancing savings will be too big to ignore. The question is still whether you can make the monthly payment on the refinance. Which path makes sense depends on your specific debt, income trajectory, and career plans, and should be worked through with your advisor and tax professional.

The Consolidation Issue

It is extremely important that this is understood. If you consolidate your pre-7/1/26 loans with a disbursement date on or after 7/1/2026, you effectively have a new loan. That means you are no longer eligible for IBR New and can only use RAP or Tiered Standard. For someone pursuing forgiveness via IBR New, this simple item could greatly increase your total loan cost.

2026 Graduating Class Examples

$500,000 in loans, no plan to own a practice. At an associate income around $200,000, the math will not work for paying off federal loans inside the system. Refinancing solves the rate, but a 20-year term at 5% on $500,000 is over $3,300 a month, which is hard to absorb early on. IBR New is usually the stronger option here: make the low payment, save monthly into a taxable brokerage account for the tax bomb (the forgiven balance is taxed as income in the year it is forgiven), and ride it out.**

$500,000 in loans, expecting to own a practice in roughly six years. Associate income until then, then a step-up after the acquisition. IBR New probably makes the most sense until you purchase the practice. After the purchase, your income should support a refinance into a fixed private rate over a manageable term. The reason I don't automatically jump to RAP to capture the interest subsidy is the risk that you don't buy a practice and your income doesn't ramp up; you would then lose six years of forgiveness progress and have to start over.

$325,000 in loans, expected income of $300,000 or higher. The sweet spot. The federal payoff math works at this loan-to-income ratio, so refinancing for a lower rate or shorter term is on the table. If practice ownership is in your future, be cautious about refinancing before purchasing the practice, as it could affect your approval.

This is also where the RAP plan might have appeal. The way RAP is structured, if your payment is below the monthly interest charge, the remaining interest is credited, so your loan balance isn't growing. For example, on $325,000 at 8%, year one your payment could be the $10/month minimum based on your prior-year tax return, which would credit roughly $26,000 of interest in that first year alone (illustrative; based on the proposed RAP interest-subsidy structure). As mentioned, extreme caution must be taken here, since your RAP IDR credits do not transfer should you end up not refinancing.

Additional Tuition Needed: Borrower Example

Starting a tuition-based residency with $500,000 in dental school loans and $200,000 needed for residency. When you take out a federal loan after 7/1/2026 for your residency, you are restricted to RAP, Old IBR (pre-7/1/26 loans), or Tiered Standard when you graduate. Back to the basics: if you do not make enough post-program for a refinance to be feasible, you are tracking toward forgiveness.

By taking out a federal loan after 7/1/26, your forgiveness term post-graduation is 30 years on RAP, not 20 with IBR New. Yes, you would need to pay back more in private loans (the amount borrowed above the federal limit), but you have much more flexibility on your repayment plan options.

This is where there may be a small window for a planning opportunity. If you are at the tail end of your program with a high federal balance, you could consider taking out private loans only to finish your program, which could preserve your IBR New eligibility.

Optimally, you would make enough money post-residency that a refinance is the ideal path, but understanding the choices you make now and how they affect repayment flexibility is important.

Overall Takeaway

The student loan situation has become extremely complex, and every party proposes a solution that just makes it worse. You can optimize your strategy now, but what happens when new rules come out under whoever is in charge next? If it makes sense, refinancing at some point is the way to escape the cycle. For some of you, your debt levels and income limit that option. That is okay; we just need to work through the options. The worst thing you can do is ignore your situation or wait until your group chat tells you what to do.

KEY TAKEAWAYS

• Career path, income, and interest rates — all affected by timing — drive every student loan decision.

• RAP IDR credits do not transfer to other plans, and borrowing or consolidating after 7/1/2026 can cost you IBR New eligibility. The choices you make at graduation matter.

• When the numbers work, refinancing can save meaningfully — but it forfeits federal protections, so weigh it carefully with your advisor and tax professional.

Next Steps

For those of you who purchased your disability insurance with us, your student loan analysis is included. We will reach out to schedule your new-grad onboarding meeting in the fall and your annual review in 2027. Please take advantage of this.

For those who want to learn more about working with us, you can schedule a complimentary consultation, or explore our $59/month New Grad/Resident planning option.

Not sure which plan fits your situation? Every D4 has a different mix of loans, income trajectory, and career path. Let's walk through yours together — reach out and an advisor will follow up to schedule time.

Virtus Financial Partners is a registered investment advisor specializing in comprehensive financial planning for dental professionals. The firm serves clients nationwide from its office in Winter Park, Florida.

* Rates are subject to change and individual results vary. The interest rate dictates the total cost of your debt.

** Investing in a taxable brokerage account involves risk, including the potential loss of principal. Investment returns are not guaranteed and may not be enough to cover the tax liability at forgiveness. This strategy should be evaluated with your financial advisor.

Virtus Financial Partners is an investment advisor registered with the U.S. Securities and Exchange Commission. Any statement of past performance is not indicative of future returns. Virtus does not provide legal or tax advice. You should consult with your attorney or tax professional for any advice pertaining to legal and/or tax questions you have.